The European BASE24 User Group (EBUG) was established in the 1980s as an independent, community-led organization for users of the BASE24 payment processing system developed by Applied Communications, Inc. (now ACI Worldwide).

Originally a regional forum for IT professionals in Europe to discuss HPE NonStop (Tandem) transaction monitoring and network security, the group expanded globally over time.

attended EBUG, booth in 2007 –

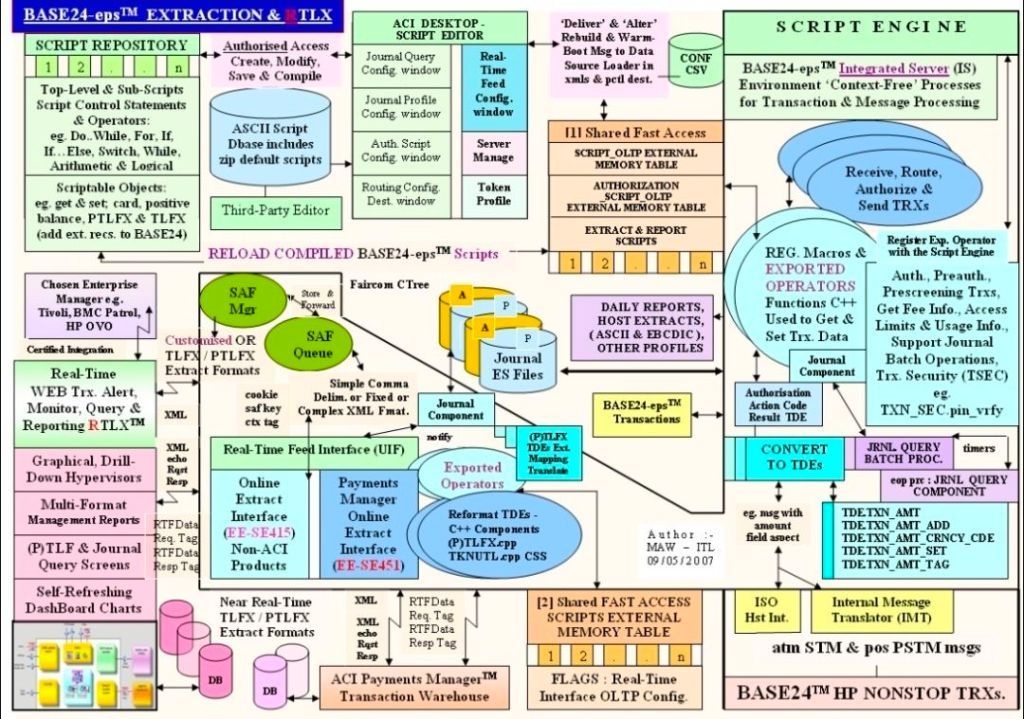

RTLX now ETI-NET C-Deep

Following ACI’s withdrawal of direct corporate backing, EBUG evolved into “The Independent Group for All Payments System Users”—affectionately known as the Everybody Belongs User’s Group—welcoming users of multiple payment platforms like Postilion.

The detailed historical timeline of EBUG and the evolution of its core system, BASE24, outlines its development from a regional user collective to a global payments forum:

The Foundation Era (1975–1989)

- 1975: ACI is founded in Omaha, Nebraska, initially developing software for fault-tolerant Tandem NonStop computers to connect ATMs to bank networks.

- 1982: The BASE24 product family is officially launched globally, acting as “baseline” software for 24-hour financial operations.

- 1980s: EBUG is established as a regional European community for BASE24 users to collaborate on ATM networking and transaction processing.

- 1986: ACI expands BASE24’s reach, reporting 131 customers across 14 countries.

EBUG Prestige & BASE24 Transformation (1990–2009)

- 1995: ACI goes public, trading on the Nasdaq stock exchange.

- Early 2000s: EBUG annual conferences grow in prestige, featuring technical tracks on BASE24 transaction logging, Point-of-Sale (POS) networks, and network resilience.

- 2007: EBUG hosts a high-profile international conference in Istanbul, Turkey.

- 2008: EBUG hosts its annual meeting in Vienna, Austria, which is historically noted as a pivotal year where ACI began supporting immediate payments in Europe and discussed a strategic shift toward IBM platforms. ACI officially announces the future retirement of “BASE24 Classic”.

- 2009: The conference is held in Prague, Czech Republic, maintaining strong community support for BASE24 on Tandem servers despite broader industry shifts.

Global Expansion, Rebranding & The Cloud Era (2010–Present)

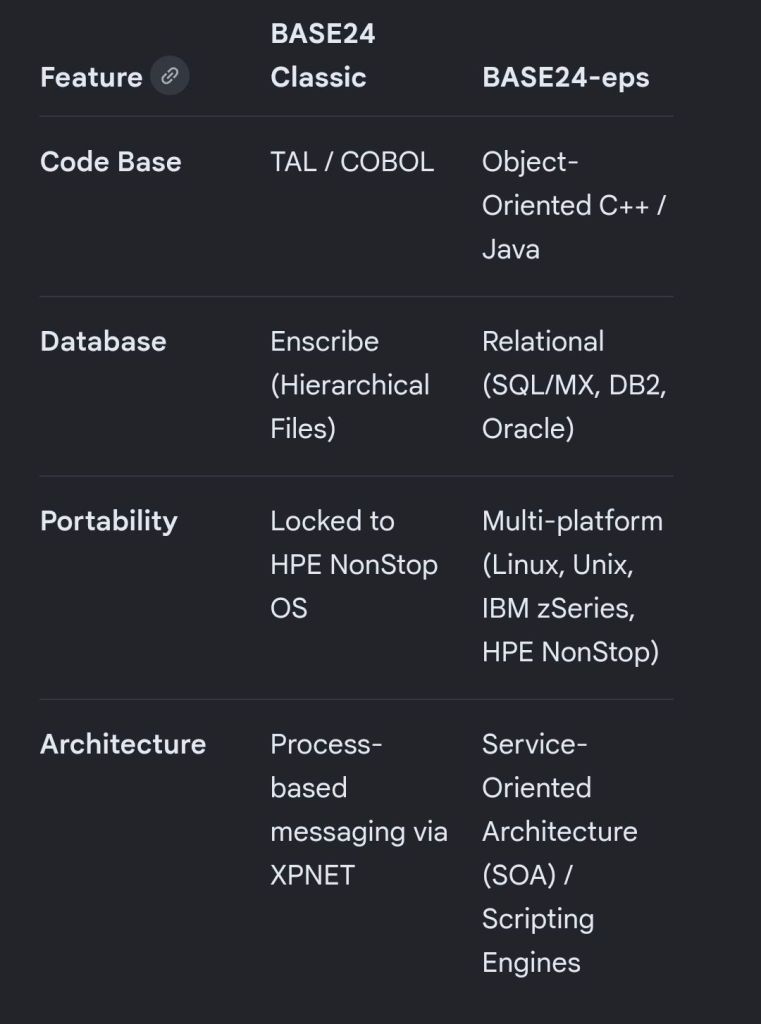

- 2012: ACI introduces BASE24-eps, their next-generation, platform-independent payments engine designed to replace the legacy BASE24 on HPE NonStop. EBUG’s technical focus shifts to real-time payments and log extraction.

- 2013: With ACI ending direct involvement, the user group officially rebrands as the “Everybody Belongs User’s Group” at their conference in London, expanding attendance to professionals from Mexico, South Africa, and Australia.

- 2015: ACI celebrates 40 years in payments. EBUG solidifies its status as a supplier-agnostic payments forum, opening sessions to non-BASE24 users.

- 2020s: With BASE24 Classic retired, legacy users migrate to modern systems like BASE24-eps for cloud deployments and immediate payments.

- Recent Years: ACI goes live as a pioneer in the Federal Reserve’s FedNow Service, building upon the decades-long transaction switching architecture first developed in the 1970s and 1980s.

European BASE24 User Group (EBUG) Timeline from Inception