In professional project management and construction, cost estimating and cost planning are complementary processes that occur at different stages to ensure a project remains financially viable.

1. Cost Estimating: “What will it cost?”

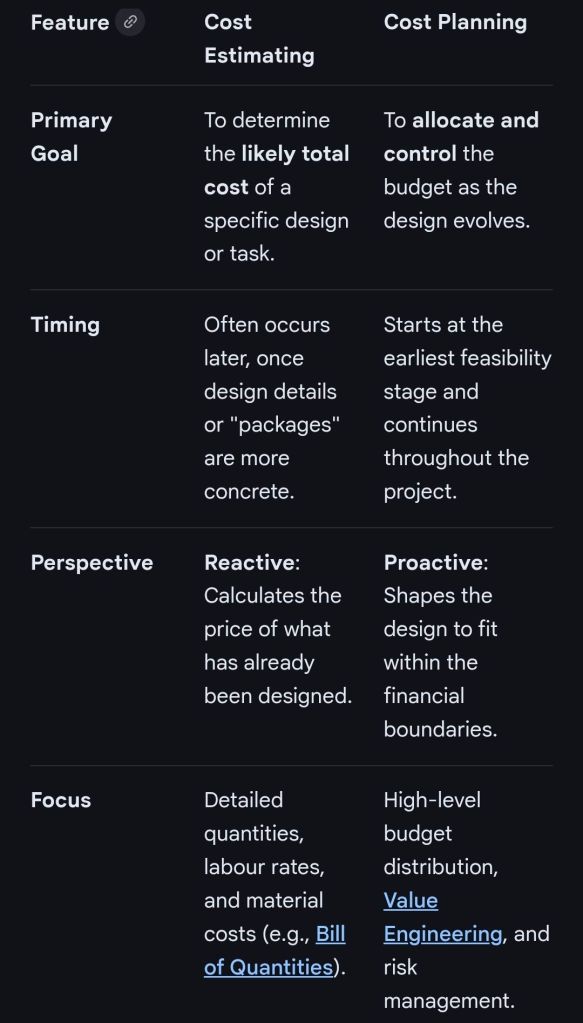

Cost estimating is a technical assessment used to predict the expenditures for a project.

- Early Stages: Estimates might be “rough orders of magnitude” based on square footage or historical data (e.g., cost per hotel room).

- Later Stages: Estimates become precise “tender figures” used by contractors to bid on work, factoring in current market rates for labour and materials.

- Function: It answers the question: “Is this specific plan affordable?”.

2. Cost Planning: “How do we stay on budget?”

Cost planning is a strategic framework that manages a project’s financial health from start to finish.

- Iterative Process: It is a “living document” that is updated as the project moves from concept to detailed design.

- Allocation: It breaks down the total budget into “elemental” targets (e.g., spending £X on the foundation and £Y on finishes).

- Control: If an estimate for one part of the project exceeds its target, the cost plan guides the team to adjust the design or find savings elsewhere to keep the overall project on track.

Standard Professional Guidance

The Royal Institution of Chartered Surveyors (RICS) provides the New Rules of Measurement (NRM 1), which standardises how these processes work together:

- Order of Cost Estimate: Establishing the initial viability of a project.

- Elemental Cost Plan: Breaking the estimate down into functional parts.

- Cost Checking: Continually comparing design changes against the cost plan to prevent overspending.